Client Login

Client Login Contact us

Contact us

5 smart investing strategies

When it comes to investing, there’s no shortage of theories, approaches, and ideas. Visit a bookstore or search online and you may be overwhelmed with information.

Five Smart Investing Strategies attempts to simplify the investment process. We’re going to review five strategies and show how they can help guide your approach to the financial markets.

While there is much to learn about how markets operate and function, understanding a few sound strategies may be enough to help you get started on the process.

Let’s take a closer look at market timing.

Market timing is an attempt to follow one of the oldest maxims in investing: “Buy low and sell high.” As the illustration shows, perfect market timing would require you to buy when the market “bottoms,” and to sell when prices near their “peak.”

However, it’s difficult to know when the market is about to turn higher or lower. All too often, investors buy as the market is reaching its peak—when enthusiasm in the market is highest—then sell after a steep drop.

Investors who attempt to time the market can have success over the short term. However, over the long term, it can be a difficult strategy to follow.

This illustration is a hypothetical example. It is not representative of any investment or combination of investments. Actual results will vary.

The cost of market timing can be high.

The chart above shows that the Standard & Poor’s 500 Composite Index (total return) had an average annual return of 7.68% for the 20-year period starting January 1, 1995, through December 31, 2015. However, investors who missed the five best trading days during that 21-year period had an average annual return of 5.49%. Investors who missed the 10 best trading days had an average annual return of 4.00%. And investors who missed the 20 best days had an average annual return of 1.57% over the 20-year period.

Are we suggesting all investors stay in the stock market all the time?

Certainly not. However, the chart does show that missing the market’s best days can have an influence on overall return. Keep in mind that the return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost.

Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

Source: Index Fund Advisors, March 28, 2017 (Latest data available.)

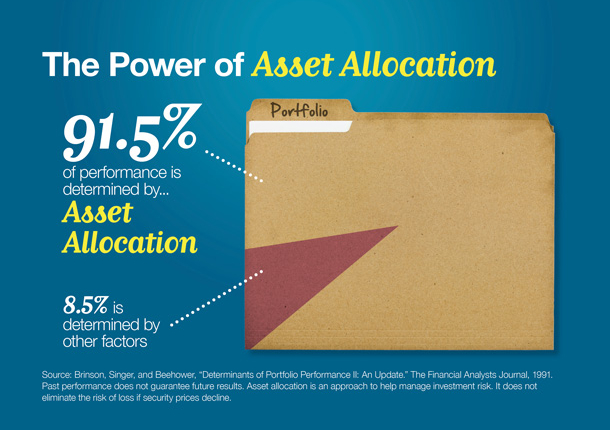

Another investment strategy that has the potential to influence a portfolio’s overall return is asset allocation.

Asset allocation is an approach to manage investment risk by diversifying a portfolio among major asset classes, such as stocks, bonds, and cash alternatives. Stocks, bonds, and cash alternatives have different levels of risk and potential return. Over any period of time, one asset class may be increasing in value while another may be falling. Both asset allocation and diversification are approaches to help manage investment risk. They do not guarantee against investment loss.

One landmark study showed that up to 91.5% of the performance of an average portfolio is determined by how the assets within that portfolio are allocated between different investment classes. Only 8.5% has to do with the specific securities chosen. Past performance does not guarantee future results.

Source: Brinson, Singer, and Beebower, “Determinants of Portfolio Performance II: An Update.” The Financial Analysts Journal, 1991.

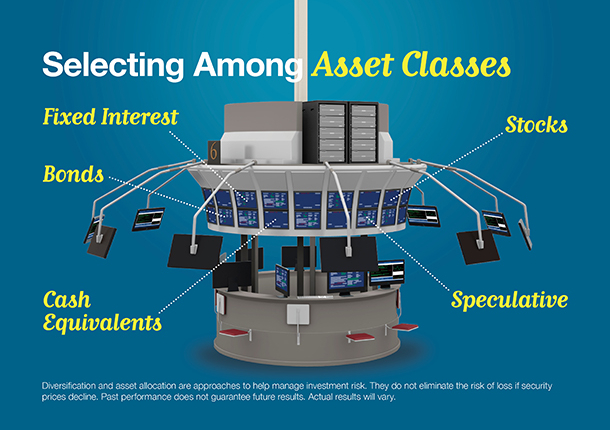

Asset allocation can have such a strong influence on a portfolio’s overall return. Here’s a look at each major asset class.

Cash equivalents are investments that are readily convertible into cash. Some consider money market mutual funds a cash equivalent. Money market funds are not insured or guaranteed by the FDIC or any other government agency. Money market funds seek to preserve the value of your investment at $1.00 a share. However, it is possible to lose money by investing in a money market fund. Money market mutual funds are sold only by prospectus. You should consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

Fixed-income tools are vehicles that offer fixed payments. Some fixed-income tools have contract limitations, fees, and charges, including account and administrative fees, underlying investment management fees, and mortality and expense fees. They may also have surrender fees if you withdraw the money in the initial years. Bonds are debt investments that are issued by federal, state, and local governments, government agencies, and corporations. Those who invest in bonds receive interest payments until the bonds mature, at which time the investors’ original principal is repaid, barring a default by the issuer. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing bonds typically falls. If an investor sells a bond before maturity, it may be worth more or less than the initial purchase price. Investments seeking to achieve higher yields also involve a higher degree of risk. With stocks, the return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk. Finally, we have more speculative investments. These types of investments can be attractive due to their high potential return. But high return also can have severe downside potential. These types of securities may not be suitable for everyone.

With a basic understanding of asset classes, the next step is the selection process—allocating assets among the major classes. The problem is that within the major asset classes, there are thousands of investment options. Many wonder where to begin.

The best place to start is to consider your investment goals, risk tolerance, and time horizon. If your time horizon is less than three years, certain asset classes may be more appropriate than others. If your time horizon is 20+ years, you may be able to consider a wider spectrum of asset classes.

Let’s take a closer look at the long-term performance of three major asset classes: cash alternatives, bonds and stocks. As the illustration shows, over the 20-year period, stocks were the best performing asset class. However, stock prices were volatile over that period of time, which may not appeal to investors with a lower risk tolerance.

Cash alternatives had a steady return over the 20 years, but underperformed the other two asset classes. Conservative investors who kept all their assets in cash alternatives didn’t experience the market volatility, but also realized a lower return and may have lost purchasing power due to inflation.

Stocks posted a better return than bonds during the 20-year period. But stocks also were more volatile than bonds.

Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market. Cash is represented by the Citigroup 3-Month Treasury-Bill Index, an unmanaged index that is generally considered representative of the U.S. cash market.

Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate.

Source: Thomson Reuters, 2018. For the period January 1, 1998, to December 31, 2017.

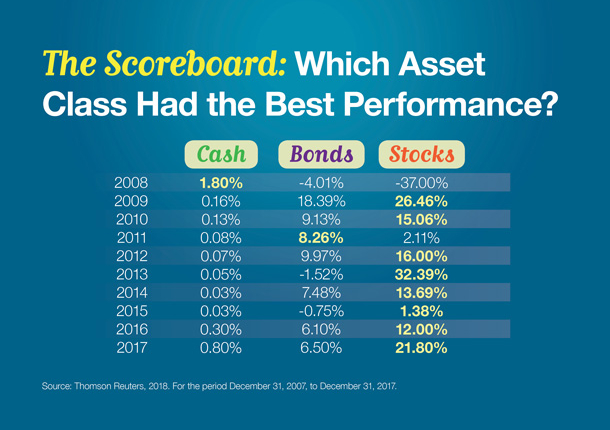

When you look at the short term, the top-performing asset class can change from year to year.

In 2008, cash had the top average annual rate of return. In 2009 and 2010, stocks fared best. In 2011, bonds took top honors. Finally, for 2012 through 2017, stocks won out.

Over any one-year period of time, one asset class may be increasing in value while another may be falling in price. By allocating assets among investment classes, investors are looking to generate the highest potential return based on their investment goals, risk tolerance, and time horizon. However, asset allocation is an approach to help manage investment risk. It does not guarantee against investment loss.

Stocks are represented by the S&P 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market. Cash is represented by the Citigroup 3-Month Treasury-Bill Index, an unmanaged index that is generally considered representative of U.S. cash market.

Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate.

Source: Thomson Reuters, 2018. For the period December 31, 2007, to December 31, 2017.

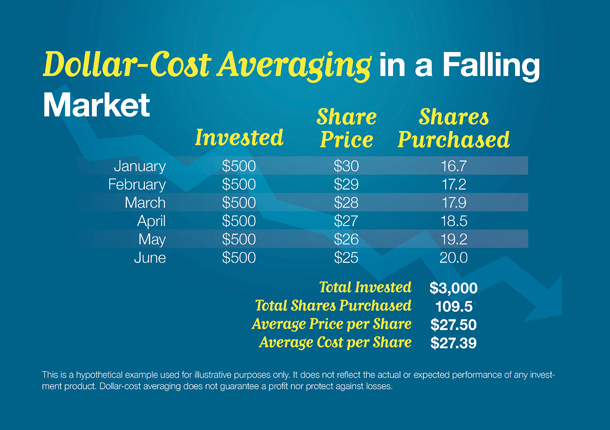

The next investment strategy to review is dollar-cost averaging, which involves systematic investment of a fixed amount at regular intervals. Instead of trying to time the market, you’re investing on a regular schedule. That means you’re automatically buying more shares when share prices are lower and fewer when they are higher.

For example, if you were to invest $500 per month into an investment whose price per share was falling, at the end of six months you would have invested $3,000 and purchased 109.5 shares. A bit of quick math reveals that your average price per share was $27.50 but your average cost per share—the price you actually paid—was only $27.39.

Keep in mind that dollar-cost averaging does not protect against a loss in a declining market or guarantee a profit in a rising market. Dollar-cost averaging is the process of investing a fixed amount of money in an investment vehicle at regular intervals, typically monthly, for an extended period of time, regardless of price. Investors should evaluate their financial ability to continue making purchases through periods of declining and rising prices. The return and principal value of stock prices will fluctuate as market conditions change. Shares, when sold, may be worth more or less than their original cost.

This is a hypothetical example used for illustrative purposes only. It does not reflect the actual or expected performance of any investment product.

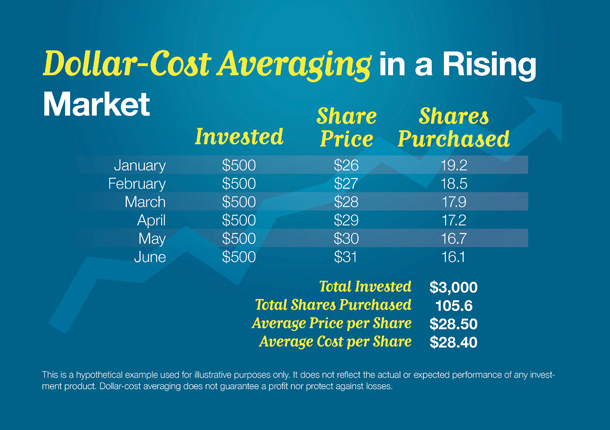

Does the same principle work in a rising market?

As the illustration shows, if you were to invest that same $500 per month into an investment whose price per share was rising, at the end of six months you would have invested $3,000 and purchased 105.6 shares. The average price per share was $28.50 but the average cost per share—the price actually paid—was only $28.40.

Dollar-cost averaging is a long-range plan. An investor is looking to benefit from what is called “averaging.” The strategy helps maintain a disciplined investment approach despite any nerve-racking swings in the financial market. When others may be tempted to give up on the market, investors that practice dollar-cost averaging invest a specific amount at a regular interval.

Dollar-cost averaging does not protect against a loss in a declining market or guarantee a profit in a rising market. Dollar-cost averaging is the process of investing a fixed amount of money in an investment vehicle at regular intervals, typically monthly, for an extended period of time, regardless of price. Investors should evaluate their financial ability to continue making purchases through periods of declining and rising prices. The return and principal value of stock prices will fluctuate as market conditions change. Shares, when sold, may be worth more or less than their original cost.

This is a hypothetical example used for illustrative purposes only. It does not reflect the actual or expected performance of any investment product.

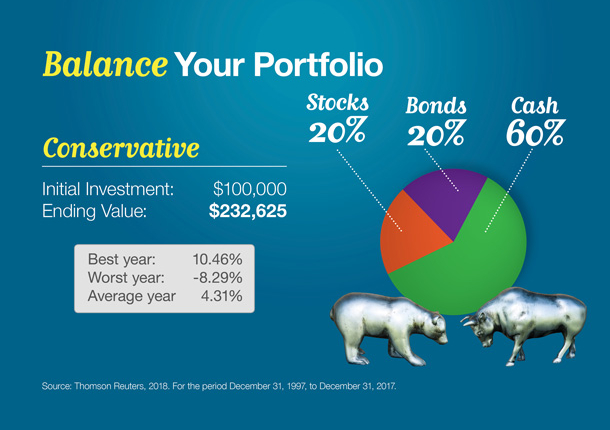

The final area to cover is balancing your portfolio.

In this illustration, an investor created a more conservative portfolio. The investor’s $100,000 portfolio was allocated 60% to cash equivalents, 20% to bonds, and 20% to stocks.

For the 20-year period ended December 31, 2017, the hypothetical portfolio generated an average annual rate of return of 4.31%. The investor’s initial $100,000 investment increased to $232,625. In its best year, this portfolio posted a 10.46% annual return. In its worst year, it would have lost -8.29%.

Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market. Cash is represented by the Citigroup 3-Month Treasury-Bill Index, an unmanaged index that is generally considered representative of the U.S. cash market.

Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate.

Source: Thomson Reuters, 2018. For the period December 31, 1997, to December 31, 2017.

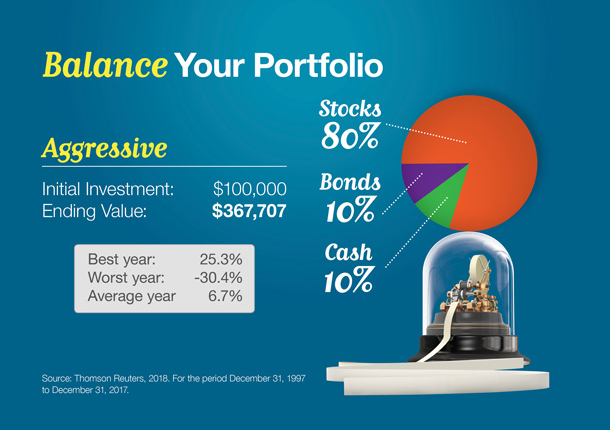

In this illustration, an investor created a more aggressive portfolio. The investor’s $100,000 portfolio was allocated 80% to stocks, 10% to bonds, and 10% to cash.

For the 20-year period ended December 31, 2017, the hypothetical portfolio generated an average annual rate of return of 6.7%. The investor’s initial $100,000 investment increased to $367,707. In its best year, this portfolio posted a 25.3% annual return. In its worst year, it would have lost -30.4%.

Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market. Cash is represented by the Citigroup 3-Month Treasury-Bill Index, an unmanaged index that is generally considered representative of the U.S. cash market.

Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate.

Source: Thomson Reuters, 2018. For the period December 31, 1997, to December 31, 2017.

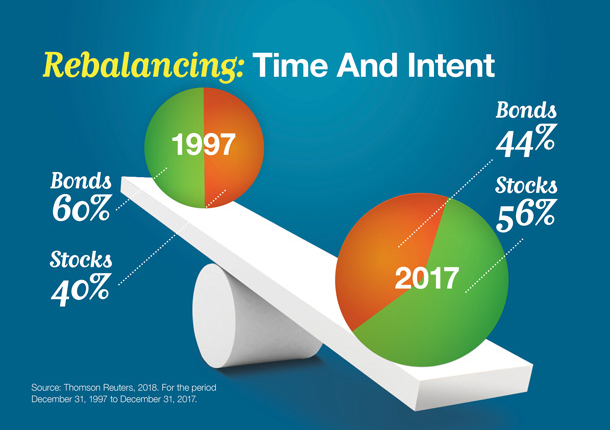

Balancing is not a one-time event. It’s an ongoing process. That’s because time can change your portfolio’s profile. If overlooked for a period of time, a portfolio may take on a completely different degree of risk.

For example, consider a hypothetical portfolio started December 31, 1997, with a balance of 50% bonds and 50% stocks.

What would the portfolio look like on December 31, 2017?

It would have shifted to 44% bonds and 56% stocks. That’s more aggressive than the original intent. And that’s where rebalancing comes in. Periodically rebalancing your portfolio may help it continue to reflect your intent and risk tolerance.

Stocks are represented by the Standard & Poor’s 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market.

Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index.

The rate of return on investments will vary over time, particularly for longer-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate.

This is a hypothetical example used for illustrative purposes only. It is not representative of any specific investment or combination of investments.

Source: Thomson Reuters, 2018. For the period December 31, 1997, to December 31, 2017.

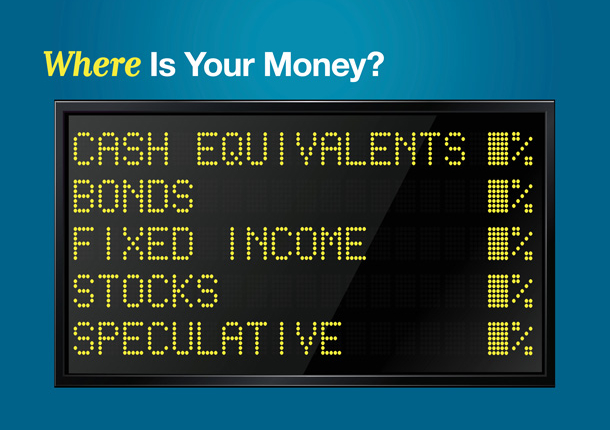

Here’s an interesting exercise to get you started.

It’s a valuable look at where you are.

We’ve just seen a series of pie charts that showed hypothetical portfolios; what does your investment mix look like? Where is your money invested right now?

Make sure you account for all your investments. That would include your rainy-day funds, the money set aside in your qualified retirement plans, everything.

Many find this exercise to be a bit difficult. They’ve never thought about their investments by asset class before—let alone tried to figure out how well balanced their investment approach is and whether it’s consistent with their investment objectives, tolerance for risk, and time frame.

Yet it can be critical. If you don’t know where you are, how can you map a path to where you’d like to be?

Putting together a sound investment strategy can make your investment efforts much more effective. But it doesn’t end there. Effective investing requires an ongoing effort. And there’s a lot more to know.

Here are some questions that arise at different stages of life:

Anthony and Selena have a growing family and wonder, “What’s the fastest way to amass enough money to buy a vacation home?”

Dave and Christine are in retirement. They ask, “How do we shift our investments to generate more income?”

Rebecca is a single woman with a small business. She wants to know, “How should my business affect my investment decisions?”

Isaac likes to do research online. He asks, “The market’s been volatile; should I increase or decrease my stock holdings?”

Answers will depend on each unique situation.